Deciding when to start collecting your Social Security benefits is one of the most complicated and consequential decisions in retirement. The difference between a good decision and a poor one could cost you and your spouse tens of thousands of dollars over your retirement, so doing your due diligence when or before you turn 62 is a smart move.

Factors to Consider

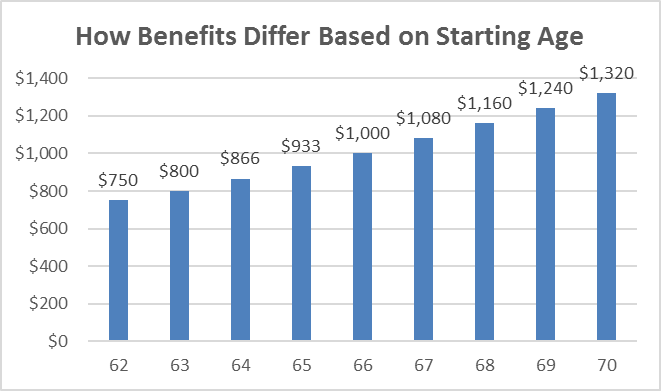

You can claim Social Security any time between the ages of 62 and 70, but each year you wait increases your benefits between 5 and 8 percent. However, there are other factors you need to consider to help you make a good decision, like your health and family longevity, whether you plan to work in retirement, along with spousal and survivor benefits.

To help you weigh your claiming strategies, you need to know that Social Security Administration claims specialists are not trained or authorized to give you personal advice on when you should start drawing your benefits. They can only provide you information on how the system works under different circumstances. To get advice you’ll need to turn to other sources.

Online Tools

Your first step in getting Social Security claiming strategy advice is to go to SSA.gov/myaccount to get your personalized statement that estimates what your retirement benefits will be at ages 62 through 70. These estimates are based on your yearly earnings that are also listed on your report.

Once you get your estimates for both you and your spouse, there are several online Social Security strategy calculators you can turn to that can compare your options so you can make an informed decision.

The best one that’s completely free to use is Open Social Security, which runs the math for each possible claiming age (or, if you’re married, each possible combination of claiming ages) and reports back, telling you which strategy is expected to provide the most total spendable dollars over your lifetime.

But if you want a more thorough analysis consider fee-based calculators like Maximize My Social Security or Social Security Solutions. Both tools, which are particularly helpful to married couples as well as divorced or widowed persons, will run what-if scenarios based on your circumstances and show how different filing strategies affect the total payout over the same time frame.

Maximize My Social Security’s web-based service costs $40 per year for a household, while Social Security Solutions offers several levels of web-based and personalized phone advice ranging from $20 to $250.

In-Person Advice

You may also be able to get help through a financial planner. Look for someone who is a fee-only certified financial planner (CFP) that charges on an hourly basis and has experience in Social Security analysis.

To find someone, use the National Association of Personal Financial Advisors online directory or try the Garrett Planning Network, which is a network of fee-only advisers that charge between $150 and $300 per hour.

Jim Miller publishes the Savvy Senior, a nationally syndicated column that offers advice for Boomers and Seniors.

Related Articles & Free Vermont Maturity Subscription

A Little-Known Social Security Program Helps Seniors Manage Their Money

How Social Security Works When a Spouse or Ex-Spouse Dies

How to Locate an Unclaimed Life Insurance Policy

Free Subscription to Vermont Maturity Magazine

Comment here